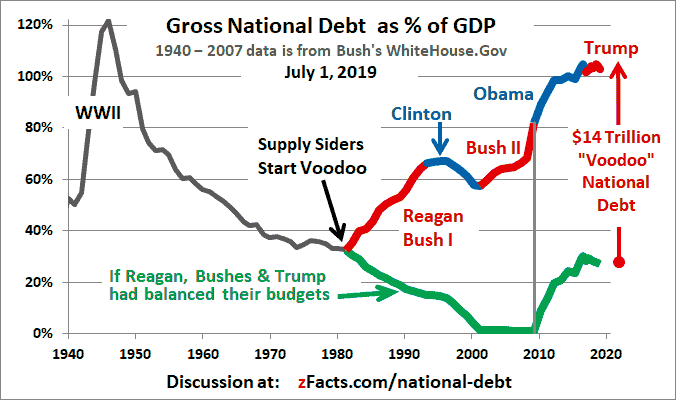

I almost titled this, “It’s the distribution, stupid,” but there’s more to it than that. A while ago I published a piece called The signature of incipient depression that pointed out the similarity of the current period (still applies, two years later) to 1929, pre-The Great Depression: namely, the very high total nonfinancial debt to GDP, and the extreme inequality of the income and wealth distributions. Today I can add declining real incomes for the ~90+ percent as the third leg of the stool.

In a consumer-based economy, effective demand collapses when most people’s real incomes are falling, as they are now. I’m putting up graphs of the three main elements of this signature of incipient depression, mostly in response to a stupid piece in Quartz from someone “refuting” Reinhart and Rogoff (here). Not that they’re wrong, or that the No Exit situation that the fiscal authorities are in won’t prevent them from blowing the biggest debt bubble in world history over the next six years as posited in When will the financial singularity occur? ~2020. Another six years might seem like a long time to kick the can down the road, but it would make this episode of ZIRP approximately as long as the previous one (1934-1946).

It is always possible for an economist—an ideological cheerleader—to miss the forest for the trees. The most powerful fiscal remedies available to us now are steeply progressive income and wealth taxes, and a program of food and shelter and basic medical care in exchange for work for the dispossessed, who may be expected to become numerous if present trends continue. Or perhaps a negative income tax with the elimination of the minimum wage. And put health insurance on a hybrid single payer system so that everyone gets at least some coverage.

The point being: The US economy still sports the signature of incipient depression. As the focus ostensibly turns to fiscal policy for the remainder of the decade I suppose the best advice is to try to get on the gravy train if you can. The next decade will be the Depression 2.0 decade, in all likelihood, the true test of democracy vs. fascism—we’re not there yet. And given how piggy the 1 percent are world-wide we might not see much inflation until about 2020 either—except of course that rolling through asset markets. My best guess is that the Feds will tase the labor market with a little more monetary tough love (also part of the “wash and rinse” cycle in the stock and metal markets, one for the Gipper, so to speak) so that the big boys can get nice and levered up for the big ramping up in asset markets to come in the second half of the decade. Ordinary working people are hosed pretty much everywhere, it seems. Just my guess.

The debt situation is worse if you look at all nonfinancial debt:

Here’s a longer-term picture of household income:

And that’s using the government’s phony hedonically adjusted inflation measure.