It is a beautiful sunny day here, and the family gathering has been relatively peaceful (I have been prohibited from talking politics).

Best wishes for whatever solstice-based holiday you're celebrating!

It is a beautiful sunny day here, and the family gathering has been relatively peaceful (I have been prohibited from talking politics).

Best wishes for whatever solstice-based holiday you're celebrating!

What do you wanna bet Janet doesn't have the cojones to taper (much)?

Wall Street will undoubtedly exert its control over the West Coaster, to get her trained.

But more importantly as John Hussman points out it is the relationship between the stock of assets on the Fed's balance sheet and GDP that matters, and a mere slowing of asset purchases won't much change that.

This confirms my view that rates will stay low for years to come, that we are following in broad outline the Thirties, and that a return to "normal" rates will not occur until a resolution of the Crisis is within sight (ZIRP persisted in the Great Depression until about 1942).

Listen up, Troika and House Republicans!

The rich rule over the poor, and the borrower is slave to the lender.

Whoever sows injustice reaps calamity, and the rod they wield will be broken.

The generous will themselves be blessed, for they share their food with the poor.

From an adaptation-level theoretic perspective, I don’t understand why confidence hasn’t collapsed already.

Source: Census via FRED. Annual data through 2012.

Two recent items on the major problem facing the world today, the explosion of inequality and the destabilization of society across the globe. The first is a graph showing that inequality has hit the “global upper middle class” the worst in relative terms (e.g., the American middle class and similars).

The great economic reshuffle – Reuters

October 28, 2013 @ 3:43 pm

By Shane Ferro

Branko Milanovic [1], the lead economist at the World Bank’s research department, has a new paper out on global income inequality (the paper was first spotted by John McDermot [2]t). Among other things, Milanovic compares the change in global income from 1988 to 2008:

[3]

He writes:

Global income distribution has thus changed in a remarkable way. It was probably the profoundest global reshuffle of people’s economic positions since the Industrial revolution. Broadly speaking, the bottom third, with the exception of the very poorest, became significantly better-off, and many of people there escaped absolute poverty. The middle third or more became much richer, seeing their real incomes rise by approximately 3% per capita annually.

And yet, those in the 75th to 90th percentile of the income distribution — including “many from former Communist countries and Latin America, as well as those citizens of rich countries whose incomes stagnated” — haven’t seen the sort of gains that the bottom half and the top 1% have. […]

The second article I’m linking to emphasizes the growth of billionaires outside the US and the West. Some might say that America’s greatest export has been its culture, not the least part of which is our glorification of greedy material acquisition. We have seen the shameless tax avoidance of the very rich across the globe—for example, Gerard Depardieu in France emigrating (at last report) to avoid a 75 percent marginal tax rate on income over about two million dollars. In American the highest growth rates occurred when wew had such marginal tax rates and there was a sense of a viable social contract, and when incomes far beyond anything needed for happiness or a good life caused a mild sense of shame among many (I know, I was there and had rich relatives who paid their taxes without complaint).

Billionaires: Decline of the West, Rise of the Rest – triplecrisis.com

Robin Broad and John Cavanagh

With the help of Forbes magazine, we and colleagues at the Institute for Policy Studies have been tracking the world’s billionaires and rising inequality the world over for several decades. Just as a drop of water gives us a clue into the chemical composition of the sea, these billionaires offer fascinating clues into the changing face of global power and inequality.

After our initial gawking at the extravagance of this year’s list of 1,426, we looked closer. This list reveals the major power shift in the world today:the decline of the West and the rise of the rest. Gone are the days when U.S. billionaires accounted for over 40 percent of the list, with Western Europe and Japan making up most of the rest. Today, the Asia-Pacific region hosts 386 billionaires, 20 more than all of Europe and Russia combined.

In 2013, of the 9 countries that are home to over 30 billionaires each, only three are traditional “developed” countries: the United States, Germany, and the United Kingdom.

Next in line after the United States, with its 442 billionaires today? China, with 122 billionaires (up from zero billionaires in 1995), and third place goes to Russia with 110. China’s billionaires have made money from every possible source. Consider the country’s richest man, Zong Qinghou, who made his $11.6 billion through his ownership of the country’s largest beverage maker. Russia’s lengthy billionaire list is led by men who reaped billions from the country’s vast oil, gas and mineral wealth with devastating consequences to the environment. […]

With this kind of concentration of wealth and power the specter of neo-feudalistic global fascism (rule by greedy corporation) is not such a stretch to imagine. Look at Europe, look at the United States.

Labor arbitrage is a game that can be played indefinitely. Until marginal tax rates on very high incomes can be raised substantially global imbalances and instability will probably increase.

Physicist Michio Kaku on how pubic protests stopped nukes from being used by Eisenhower and Nixon. Relevant today as Sheldon Adelman suggests dropping a “demonstration bomb” “in the middle of the desert” in Iran. Nothing could possibly go wrong with that, right? Think Putin might not take that as an affront to his masculinity, and require to drop on on Alaska, perhaps, or North Dakota?

Tax Rates, Inequality, and US Deficits – Barry Ritholtz. Sometimes no one nails it like Barry.

Its Friday, after what was for me a long and annoying 17 days. But the shutdown is over, US markets are at all time highs, and Bob Shiller got his Nobel (more on this tomorrow).

You might think that I would be at peace with the current state of the world, but life is never that simple. You see, I have assumed the task of explaining things which require explaining. By some quirk of fate and an odd academic background, I find myself with skills in simplifying complex matters. Whether OCD or over-compensation for some other defect, this is my lot in life. (I made peace with it long ago).

As we discussed yesterday, amongst all of the background nonsense since October 1, the noise about the deficits was not really about budget deficits at all. Rather, it was about a decidedly narrow ideology held by a small percentage of Americans. Their belief is that government should be much smaller. This is a legitimate political ideology, one that has persisted over the centuries.

Their approach to this philosophy, however, is far less intellectually honest. Rather than having a full on debate on that subject — a debate they are likely to lose — they have chosen a very different approach. This time around, they made the deficit a proxy.

Because of what I do for a living, I found this offensive. Deficits impact fixed income, an important part of portfolio planning. They impact available credit, capital for investment, in a broad and varied way. Hence, the deficit is a genuine issue, a real problem that should be addressed in a mature and responsible way. It can be easily solved using intelligent solutions, but for the ideologues in Washington DC (and elsewhere) who refuse to treat it as the basic mathematics and accounting problem it actually is. The way the Tea Party and others have treated the deficit reminds me of the approach Meredith Whitney took to Municipal Debt. Both groups are stunningly ignorant about their subjects, while possessing the skills to allow them to exploit the topic, hog the spotlight for themselves and other tangential pet issues.

The Tea Party, like Whitney, turned an important question of debt and credit and solvency into one giant PR clusterfuck.

Back to our issue of taxes (next week, I will address spending). Amongst Industrialized Nations, the United States has amongst the lowest tax rates in the world, especially for those folks (like myself) who reside at the top of the income scale.

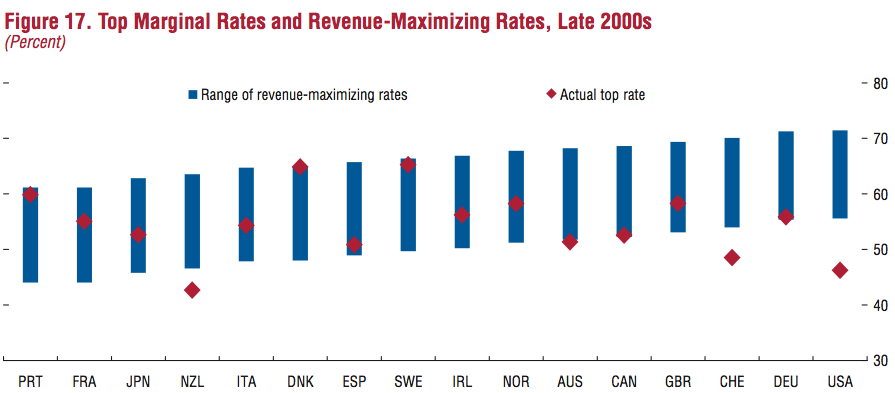

To demonstrate this, I want to point to the IMF’s World Economic and Financial Surveys: Taxing Times. It is chock full f great charts and data and other interesting results of the IMF survey.

The two below caught my eye. They are rather instructive for our discussion of taxes and deficits in the US.

The first looks at major industrial nations, and compares what the IMF calls their Revenue-Maximizing Tax Rates (blue line) versus their actual top rate (red dot).

As you can see, some countries — Denmark and Sweden — are at the top of the revenue maximizing ranges. Other countries — Canada and Germany — are at the bottom of their revenue maximizing ranges.

Then there is the United States, which is simply far off the scale, way below the bottom of its revenue maximizing range.

If your concern is deficits, than you must take notice of how much money the USA is leaving on the table. I am not suggesting that the role of government should be to maximize their tax revenues, but rather to suggest that if you want to close the deficit, you need to at least be in a defendable range. The US is not.

click for ginormous charts

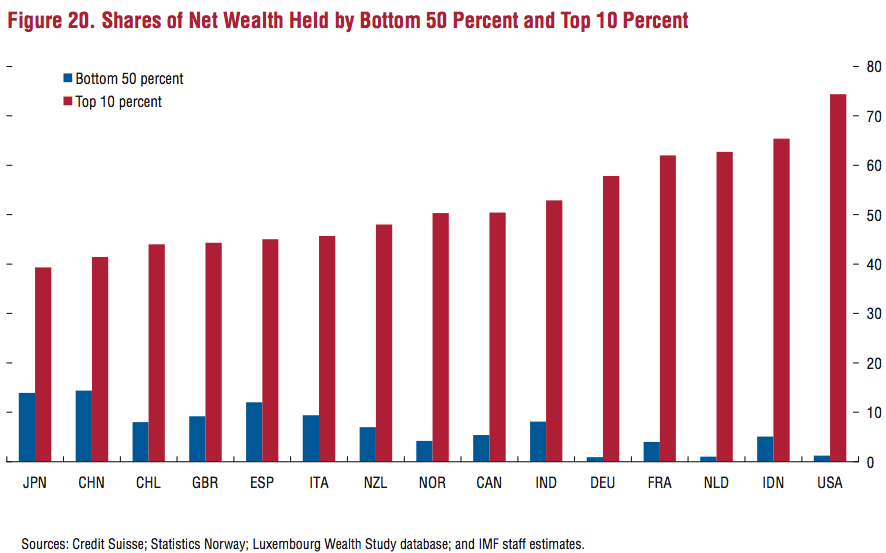

Source: IMFNot coincidentally, when we look at shares of Net Wealth held by the bottom 50% of he population versus the top 10%, the United States is off the scale. We are the most unequal nation in the world.

Source: IMFThe inescapable conclusion presented to us by this data is that our tax policy is responsible for both the world’s greatest inequality among developed nations, and our ongoing deficits.

If you have a better explanation for our current conditions, or the net results of our tax policies, I would love to hear it.

Source:

Fiscal Monitor Taxing Times

World Economic and Financial Surveys

IMF October 2013

http://www.imf.org/external/pubs/ft/fm/2013/02/fmindex.htm

Did Monetary Policy Cause the Recovery? – John Hussman. A very nice demolition of our monetary policy charade for Janet Yellen to consider. Let’s hope she has the guts to make some heads roll [i.e., to bring back honest accounting].

[…] To address this question, a proper understanding of the credit crisis is essential. Much of the present faith in monetary policy derives from the belief that it was the central factor in ending the banking crisis during what is often called the Great Recession. On careful analysis, however, the clearest and most immediate event that ended the banking crisis was not monetary policy, but the abandonment of mark-to-market accounting by the Financial Accounting Standards Board on March 16, 2009, in response to Congressional pressure by the House Committee on Financial Services onMarch 12, 2009. The change to the accounting rule FAS 157 removed the risk of widespread bank insolvency by eliminating the need for banks to make their losses transparent. No mark-to-market losses, no need for added capital, no need for regulatory intervention, recievership, or even bailouts. Misattributing the recovery to monetary policy has contributed to a faith in its effectiveness that cannot even withstand scrutiny of the 2000-2002 and 2007-2009 recessions, and the accompanying market plunges. This faith is already wavering, but the loss of this faith will be one of the most painful aspects of the completion of the present market cycle. […]

The simple fact is that the belief in direct, reliable links between monetary policy and the economy - and even with the stock market - is contrary to the lessons from a century of history. Among the many things that are demonstrably nottrue - and can be demonstrated to be untrue even with simple scatterplots - are the notions that inflation and unemployment are negatively related over time (the actual correlation is close to zero and slightly positive), that higher inflation results in lower subsequent unemployment (the actual correlation is positive), that higher monetary growth results in subsequent employment gains (the correlation is almost exactly zero), and a wide range of similarly popular variants. Even "expectations augmented" variants turn out to be useless. Examining historical evidence would be a useful exercise for Econ 101 students, who gain an unrealistic sense of cause and effect as the result of studying diagrams instead of data.

I read a lot of different blogs, mostly for their links. I have little interest in reading Yves or Michael Snyder, but they both provide lots of high-quality links, so I frequent their blogs. Some blogs I won't go to, like Brad de Long's, simply because the stench of the self-satisfied Establishment is too much.

What I find tragic about the libertarians like Mish and about the Evangelicals like Michael Snyder is that they are apparently willing to play so readily into a Government-destroying gambit that opens the way for those in control of vast wealth, the 1 percent, so to speak, to bankrupt governments worldwide and then buy up their assets at trivial prices as occurred after the fall of the Soviet Union; in other words, to take the world into the new world order dreamed of by Rockefellers and other Illuminati for generations, a neo-feudalism enforced by financial fascism through a world-wide fiat money system run by the Bank of International Settlements, which there are the lords and ladies of wealth over the debt-serfs, everyone else. Snyder even had a link to a Carroll Quigley quote on this from the Sixties.

Depression conditions are known to foster fascism, but the indicated depression conditions don't seem to bother the Evangelicals or the libertarians.

But history is nonlinear, and I maintain hope that in the Crisis to come a new viable democratic form will emerge.

http://research.stlouisfed.org/fred2/graph/?s%5B1%5D%5Bid%5D=EMRATIO

The Great Debt Illusion began with "Supply Side Economics" in Reagan I, a con game that provided definitive proof that tax cuts for the rich do not provide growth that "trickles down" to everyone else. Here's the picture of federal debt:

http://research.stlouisfed.org/fred2/series/GFDEGDQ188S

Notice where the take-off occurs. Add to this insight that it was a Republican, Nixon, who took us off the gold standard in 1971, setting the stage for massive monetization of federal debt, and it is hard not to conclude that the modern-era Republicans are the most fiscally-irresponsible party in American history. All their talk of austerity is in fact mere mean-spiritedness. This is the distinguishing characteristic of the Republican Party today.

Today, the House Republicans take pride in being the most hard-hearted folks in the country, proving it by taking their greedy frustration out on women and children by cutting funding for food stamps.

This is a party without a future.

On the employment issue: in the Sixties, it was possible to support a family on one (male) income. Not so today except for the top few percent. Multi-generational living is a growing trend, and maybe not such a bad one if it brings families closer together.

Shalom.

John Hussman has come and said what many have believed for some time now, that the Fed is probably insolvent (here).

The Fed has become the dumping ground for bad assets. Here’s what happens: they take them in from the banks at some highly notional (what is called “mark to unicorn”) value and hold them as “reserves” against the bank’s putatively active lending; which may or may not occur because the Fed now pays interest on reserves even as the reserves are likely deteriorating in value.

The Fed is the proverbial carpet under which the bad debt of the banking system is swept. Hence, the creditors and owners of banks and bank holding companies are relieved of having to recognize losses, and the fiction of “simulative monetary policy” is maintained. As Zero Hedge is fond of pointing out, the only known transmission mechanism from loose money to anything is to asset bubbles, the current one being stocks again, with a bubblet appearing in real estate.

This is capitalism without failure writ large. The antidote, in the view of the “Washington [/New York] consensus” (to borrow a term) is “more of the same.”

Like Bernanke, Janet Yellen didn’t a thing coming of the last crisis (even though the world-wide ramp-up of housing pricing made front page news in “The Economist,” as I recall.

And I can say from personal experience that many in retail banking wondered what would happen to Consumption when the housing ATM was shut off.

Thus I believe MMT will win out in the end, as war and/or infrastructure projects demand funding. Whether a major inflation or hyperinflation gets going remains an open question to me, as I believe an inflation (wage-price spiral) is a labor market phenomenon accommodated by monetary policy, and there seems little indication that the PTB have any intention of raising anybody’s wages.

Bad debts, those destined for charge-off, don’t go away by themselves; they have to be charged off. A major deflation will occur when that reconciliation finally takes place. Even if accounting fiction remains in place, the fact that such debts when returned to the banking system do not contribute revenues tells us bank margins are going to get a lot thinner in the future. A bank may be able to dress up its balance sheet but not so much its income statement.

The San Francisco Fed reports median estimate of the natural rate of unemployment in 2013 is 6.6 percent (source). Other estimates put the rate at 7.9 percent (source). Assume the current unemployment rate is the current natural rate, at 7.3 percent. How long until confidence collapses if the rate remains fixed at that level? Obviously it will take infinitely long for the adaptation level to converge to the current level, but when does it get within 0.1 of the adaptation level? That actually doesn’t occur until March 2016. But this is not a realistic path.

The crossover from “unemployment rate below adaptation level” to “unemployment rate above adaptation level”—the signal of collapsing confidence—is always preceded by a leveling out of the smoothed (12-month MA) unemployment rate, which has not yet happened. This is a necessary but not sufficient condition for a collapse of confidence to be imminent.

We will monitor developments for this occurrence.

The downtick in unemployment raised the A metric marginally but its topping formation remains in place. The onset of the next crisis of confidence—the signature characteristic of the business cycle downturn--will probably come in 2014.

As I have pointed out before, ZIRP lasted from 1934 to 1946 last time and there’s no indication it will go away soon this time. There has been less banking reform, the debt load is greater, and the distribution is even more skewed. Here is Shiller’s long term bond rate data:

Note that from 1936 to 1946 the rate went down. Data is through 2013 YTD. We are still awaiting our 1937-38 analog slump.

Unless, of course, the fools running things manage to get a big war going soon.

The next big thing, especially if Summers gets in, will be crypto-MMT debt explosion as America leaders (ruling class) feather their nests with “infrastructure spending.” Saez and Picketty showed us what happened in to the last such “growth endeavor”: it went 93 percent to the top 1 percent.

Sucks, doesn’t it? Find a faith and practice it, and congregate with like-minded people. Stay away from psychopaths (and that means almost anyone at a senior level in a large corporation, nowadays, as they are shooting the zombies climbing up beneath them in the head to protect their positions).

Peace.

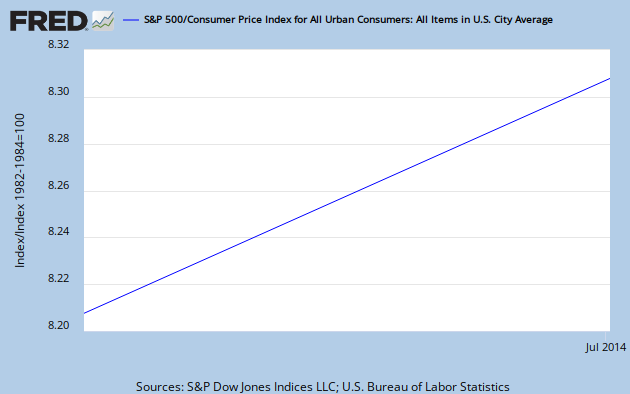

Here is a graph of the S&P 500 deflated by the CPI. Which way do you think it is going?

The entertaining Jim Quinn has put up the third in his series of "Trying to Stay Sane in an Insane World." Quinn works at Wharton and his website is either one of the cleverest honeypots around, or Wharton — a bastion of, let's face it, Wall Street think — actually allows some free speech.

However, here's my response to the Austrians who say — who chant — "Government bad! Government bad!" — and, "Free markets good! Free markets good!"

Feudalism bad! The Middle Ages were based on a system of highly concentrated ownership of the means of production, which at that time was mostly land. You had your lords and your serfs. With the assistance of rapidly improving technology are getting closer and closer to a new age of feudalism.

The Crisis still looks to peak after 2020. Buckle up.

I am pleased to recommend a new thriller, Freedom’s Sunset, which is currently in the top 50 in Amazon’s political thriller category. Please support this new author by reading the book and (if you like it) giving it a five-star review. Amazon’s algo's are very sensitive to the reviews.

Book Description

Are you concerned about the collapse of the American economy? Here is a thriller about the collapse of the Soviet empire that provides historical insight into that collapse. It is June 1990. Mikhail S. Gorbachev, President of the Union of Soviet Socialist Republics, fears that his policies of glasnost--openness--will cause the union to split apart. The Berlin Wall fell in the past November.

His political rival, Boris Yeltsin, appears to be gaining popularity. On a cold day Gorbachev comes to Minnesota in the American heartland for a historic visit. A product of the Russian countryside himself, Gorbachev is happy to be free of the intrigues of Washington, D.C. and Moscow for a day.

But he will face an encounter with Zack Pedersen, a troubled youth from South Dakota, on Summit Avenue in St. Paul that sheds light on two very different empires in different stages of collapse.

Written in a style combining John le Carré with The Hunger Games, this book will appeal to those around the world who yearn for freedom and are willing to pay the price to keep it. The story contains strong language and adult themes.

This book includes a lot biographical flashbacks on Gorbachev’s life. Reviewers find that it provides a lot of historical insight into the collapse of the USSR, and what has happened there subsequently. Gorbachev’s personal story is especially compelling.

Russia currently has a sovereign debt to GDP ratio of approximately 10-15 percent. They defaulted on much of the USSR’s debt. Putin must be laughing at the what the bankers are doing to the Europeans.

It should be evident now that "money printing" is not a sufficient cause of inflation or hyperinflation. Excess reserves pile up in the banking system and the Fed ends up "pushing on a string" with little effect on either price level or output. Hence John Williams' massive miss on his hyperinflation call. The first Great Depression taught us this.

Wikipedia helpfully defines two trigger mechanisms for hyperinflation: the "velocity" model and the "money in circulation" model. Also, please recall my fundamental definition of inflation:

Inflation is a labor market phenomenon, i.e., a wage price spiral, accommodated by monetary policy. Here I am adopting the "economics" definition of inflation as a general rise on the price level.

Now, so long as the capitalists continue to subject labor to diminishing real incomes, the only inflation that can exist is asset bubbles, financed by the increasing incomes of the capitalist class. While there is at least a feeble attempt by households to rebuild balance sheets, filling up one's gas tank with gas to beat rising gas prices does not constitute a sufficient increase in the velocity of money to trigger a hyperinflation. Fundamentally, the budget constraint on the vast majority of real incomes precludes accelerating inflation. So much for the velocity means of triggering a hyperinflation.

With the recent speculation that Lawrence Summers is the President's favorite for the new Fed chief, there is some reason to attend to the "money in circulation" model of hyperinflation. Summers is an advocate of taking on lots of new federal debt to stimulate the economy. The way that this will be accomplished may end up being a close facsimile of the Modern Monetary Theory prescriptions in that the Fed will essentially print these dollars and send them into the economy as "new money in circulation" through the Treasury. However, Janet Yellen is likely to do the same thing.

There is certainly an argument for undertaking large infrastructure projects while interest rates are extremely low. And the massive increase in debt is consistent with Sornette's estimations of the worldwide debt bubble's trajectory referenced a couple of posts ago. (Ron Paul has suggested that the Fed might simply forgive such debt held by the Fed, which would make it a pure MMT exercise.)

The point being that much of such spending might conceivably flow to the people as incomes (although the last bout of stimulus demonstrably did not, some 90+% of it winding up in the pockets of the 1%) and ignite an inflationary or hyper inflationary outcome. But I doubt it. More likely I think is that essentially carry trade-generated asset bubbles persist wherever the hot money flows, while labor's compensation remains stagnant. The vanishing middle classes around the world will experience stagflation, but not concomitantly rising wages.

Hence, Sornette's finite time singularity is likely to be profoundly deflationary when the bubble pops. There might at last be something like a global debt jubilee around 2020, simply because the debt service finally overtakes the ability of markets to absorb the debt required to pay it. This will be the End of the Modern Age, possibly, if complete monetary chaos halts much of international trade. The 2020s may be the decade when large scale barter becomes the norm between nations.

In the CIA's humint (human intelligence) areas, the study of faces is a recognized discipline. One needs to know very little about Lawrence Summers to realize he is a complete ass. The only public faces in recent memory that show such obvious bad intent are those of Phil Gramm and Paul Wolfowitz.

But it doesn't matter who is appointed to the Fed chair, because Janet Yellen will do the same thing as Summers, only possibly less aggressively.

In spite of the downtick in the unemployment rate—due to lowered labor force participation—the topping process in “animal spirits” continues; there was no break of the recent high.

As the history of the A metric shows, when it crosses the zero line from above a collapse of confidence is virtually guaranteed.

When will we get there? Frequently entry into NBER-defined recession precedes the crossing of the zero line, so my forecast of a collapse of confidence before the end of year may be plausible. Otherwise it will occur in 2014. With job growth (especially full-time, “good” job growth) at the pathetic levels it’s at, it’s hard to see how a collapse of confidence before the actually crossing of the zero line won’t take place.

Here’s a close up of my judgmental unemployment rate forecast and its attendant adaptation level forecast:

Sooner or later a lot of the unemployed are going to have to start looking for work, and that will push the unemployment rate up, precipitating the collapse of confidence as the published unemployment rate rises.

I have taken a brief look at whether coming within a “just noticeable difference” of the adaptation level is sufficient to cause the collapse, and I don’t think it is. Confidence is especially sensitive to the A metric actually attaining a negative value. However, as can be seen from the history, in many cases the NBER-defined recession occurs before that happens.

I almost titled this, “It’s the distribution, stupid,” but there’s more to it than that. A while ago I published a piece called The signature of incipient depression that pointed out the similarity of the current period (still applies, two years later) to 1929, pre-The Great Depression: namely, the very high total nonfinancial debt to GDP, and the extreme inequality of the income and wealth distributions. Today I can add declining real incomes for the ~90+ percent as the third leg of the stool.

In a consumer-based economy, effective demand collapses when most people’s real incomes are falling, as they are now. I’m putting up graphs of the three main elements of this signature of incipient depression, mostly in response to a stupid piece in Quartz from someone “refuting” Reinhart and Rogoff (here). Not that they’re wrong, or that the No Exit situation that the fiscal authorities are in won’t prevent them from blowing the biggest debt bubble in world history over the next six years as posited in When will the financial singularity occur? ~2020. Another six years might seem like a long time to kick the can down the road, but it would make this episode of ZIRP approximately as long as the previous one (1934-1946).

It is always possible for an economist—an ideological cheerleader—to miss the forest for the trees. The most powerful fiscal remedies available to us now are steeply progressive income and wealth taxes, and a program of food and shelter and basic medical care in exchange for work for the dispossessed, who may be expected to become numerous if present trends continue. Or perhaps a negative income tax with the elimination of the minimum wage. And put health insurance on a hybrid single payer system so that everyone gets at least some coverage.

The point being: The US economy still sports the signature of incipient depression. As the focus ostensibly turns to fiscal policy for the remainder of the decade I suppose the best advice is to try to get on the gravy train if you can. The next decade will be the Depression 2.0 decade, in all likelihood, the true test of democracy vs. fascism—we’re not there yet. And given how piggy the 1 percent are world-wide we might not see much inflation until about 2020 either—except of course that rolling through asset markets. My best guess is that the Feds will tase the labor market with a little more monetary tough love (also part of the “wash and rinse” cycle in the stock and metal markets, one for the Gipper, so to speak) so that the big boys can get nice and levered up for the big ramping up in asset markets to come in the second half of the decade. Ordinary working people are hosed pretty much everywhere, it seems. Just my guess.

The debt situation is worse if you look at all nonfinancial debt:

Here’s a longer-term picture of household income:

And that’s using the government’s phony hedonically adjusted inflation measure.

With U = 7.6, same as last month, the topping process in animal spirits seems to be underway. The adaptation level of U is 8.5, down 0.1 from last month. I am assuming that U will stabilize for a few months and then shoot up as self-organized criticality in the labor market kicks in. The interesting thing about this cycle, like the one in the early Seventies, is that consumer sentiment as measured by the Michigan index seems to be looking through the next slump to the next expansion already.

The political economy of the situation, in my read, is as follows: Obomba would be better off to take his recession now so that the economy is coming back in 2016 for Hillary or whoever. But the Congressional elections next year could swing radically Republican if the economy is in recession (as I expect it to be). If Ben continues to taper, he may help the Democrat in 2016, but it may hardly matter, as the Congress will have gone to the Republicans and the people may be convinced that the Democratic (and democratic) agenda has failed, and they will opt for a “strong leader.”

The one thing Republican administrations are really good at is shutting the economy down (reference). But would be consistent with their ultimate agenda of bringing feudalism back to the Western world, IMHO.

And since Ben is a servant of Wall Street, which today favors the Republicans, he will continue with the taper, executing a “wash and rinse” cycle on the stock and bond markets similar to that of the early Seventies. The inflation gets going in a few years, along with a perhaps MMT-validated increase in deficit spending (see Warren Mosler’s profile in the NYT here), which is all of course consistent with my and others’ hypothesis of a credit super nova yet to come, as the sovereigns, slaves to the banks (at least in the West), compete in a race to debase. We have Sornette’s forecast of the date for the phase transition in to what can only be a world-wide deflation as about 2020. And all this is consistent with the very prescient prophecies of Strauss and Howe in the The Fourth Turning.

Interesting times.

P.S. I am still unemployed, so anyone knowing of opportunities for a non-derivatives oriented finance geek, please let me know.

Didier Sornette has some great stuff out now. See his Ted talk and this white paper, “The Illusion of the Perpetual Money Machine,” in which he he pretty well demolishes the con game that the economics profession—slave to Wall Street—has been playing at the great expense of the people of the world. I’ve written previously about the faster than exponential growth theory of singularities, financial and otherwise (see here).

The bad debt will be cleared. Sornette indicates that his models show that the anticipated phase transition out of the growth era, originally forecast for 2030-2060 in his work with Johansen, has begun.

Andrew Jackson’s last words before dying were, “I killed the Bank!”

Where is our Andrew Jackson?

N.B. The following is research, not investment advice. You invest at your own risk, unlike the Wall Street banks, who also invest at your risk.

The Coppock curve is tracking downward.

The Coppock curve sends a long-term bottom signal when it turns up from a negative reading. Assuming the curve does not bounce up again—anything is possible but it has only bounced from this low before once, in 2012—how long until the next major market bottom? The mean number of months from a similar Coppock value ~67 to the next bottom (the signal in 2001 was the only false positive and is ignored, taking the second signal in 2002 as the true signal) was 11.6 months, with a max of 19 and a min of 5.

So the average expectation would be for a bottom in the summer of 2014, a very crude second degree polynomial fit to the the series of signal leads gives a lead time of ~8 months for a bottom in spring 2014, which has a certain harmonic resonance with the Seventies big bottom which was in March 1974.

By the way, long interest rates rose all the way up to the bottom in 1974—and beyond, of course. However, if the world economy hits an air pocket (failure of effective demand) we could see stock prices falling and further disinflation or deflation. Remember, the last ZIRP lasted from 1934 to 1946, a dozen years. It could be 2021 before short rates rise. It is really hard for me to imagine a scenario where inflation takes off except for isolated supply shocks in the current environment.

Pushing on a string seems to work for the stock market, if not the economy.

Running at about 70 percent of GDP, consumption has been above long-term averages for a while, with much of it financed by debt. Households are deleveraging where they can. Where will consumption go?

Of course, for the majority of consumers, the weakness in real disposable income has been greater than depicted because of the great degree of inequality in the income distribution. Government spending won’t pick up the slack, and neither will investment, from all appearances:

Robb has been posting a lot this month, with the Snowden disclosures. He shares my view that the nation state, while weakening, is entering a regime of “positive control” of the population that is roughly equivalent to neo-feudalism, a view I first expressed in 2009 in “On the coming neo-feudalism,” linked to by Yves at www.nakedcapitalism.com.

Start with http://globalguerrillas.typepad.com/globalguerrillas/2013/06/the-nsa-story-and-the-negative-security-it-delivers-to-everyone.html and follow the forward links to get John’s take on things. I have added him back to my list of blogs I follow.

Here is my current “big picture”:

Unless the corporations, which are the dominant form of social organization on the planet, naturally adapt according to the principles suggested by Wilkinson et al.’s findings, i.e., that it will be optimal for them to flatten the income distribution within their structures as it will lead to lower health care costs as well as productivity improvements—if there is no natural countervailing movement toward greater equality of outcomes (and I am assuming here that the rich continue to “own” the politicians, so that no reform via taxation is possible), then we have the following probable sequence: neo-feudalism + “free market” capitalism + bought-and-paid-for government by the 1% + insatiable greed triggered by great wealth => immiseration of the proletariat and Marx’s revolution—with either true social reform following or a very bloody suppression indeed by the forces of “positive control” with a rinse and repeat cycle.

There certainly is the possibility of a dystopian future ahead. The passivity, and—I will say it—the lazy stupidity of the American people make it much more probable to happen. What can you do, if demonstrating in the streets is likely to get you sent to jail and the unemployment lines? Give money to progressive organizations that are reputable. Support local efforts to expose corrupt politicians.

The only person offering a solution to the larger “bootstrapping problem” of reforming American democracy that I can see is Lawrence Lessig, whose “money bomb” idea is as follows: raise X hundreds of millions of dollars from billionaires who are committed to reform and use it to secure the election of reformers to the House and Senate, whose charge is to push through legislation to get the money out of politics, or to vastly reduce its power. See Lessig with Bill Moyers.

Former Republican presidential candidate John Huntsman referred to the American campaign finance system as “an abomination.”

I continue to view this period as very similar to 1973, with recession imminent (technically defined; we are actually in a low grade depression). The blue forecast line in the graph below is judgmental.

In A phase space, it is clear that we are turning the corner into the downturn; it is only unclear how much longer the Fed can prop it up. We are at the point A = 1.5, Delta A (YOY change) = 0.8 on the graph below, which shows four decades of history. The slide downhill comes next, whether late this year or several years from now, it is hard to tell. There is no forecasting involved other than assuming the A attractor is relatively stable. This is really just to say that “the law of the business cycle has not been repealed.” I just find it hard to believe that with the incomes of roughly 90 percent of the American population falling in real terms, that even with the extraordinary lack of labor force participation recently, that a recession can be avoided in the near term. Perhaps we’ll have a recession without an increase in unemployment (in the sense of two or more quarters of negative real growth). Whether the NBER in its wisdom would find that to be a recession is totally irrelevant. What I am forecasting is the collapse of confidence that always accompanies the business cycle downturn, and I do believe people will be smart enough to smell the coffee at some point regardless of the published unemployment rate. Times are changing.

The adaptation level is now at 8.6 percent unemployment. Any uptick to within a “just noticeable difference” of that number will probably signal imminence of further decline. Just rising above 8 percent will probably have psychological significance.

I read the attack on paper gold as a harbinger of things to come. There is a lot of liquidity looking for a buy point. TPTB might decide a quick, “controlled” rout is in their interest.

I only link to stuff anymore that really got me off. Here's Bruce Sterling's take on the unholy symbiosis of the high tech startup society and the new international Money Lords who are driving the middle class out of existence, delivered at a design conference in Berlin. He just nails it (sorry for the messy link, but I'm doing this on an iPad and don't know all the commands):

When will a global conscience arise? There is no evidence of it among most of the Money Lords.

H/t boing boing via Ritholtz

If you didn't catch this on Mish, it is must-see. Link is below. In case you had any doubt about the rot pervading Washington and Wall Steet.

http://www.youtube.com/watch?feature=player_embedded&v=7VOWnnEphjI

I posted this over at macrofuge.com:

In story form: when financial capital (ownership of “physical capital” aka the means of production) becomes too concentrated, a “failure of effective demand” occurs as the owners of the means of production lower wages to the point where consumption spending begins to fail; this depresses “animal spirits” quite rationally because most [true] investment demand is a derived demand (from consumer demand); hence the preference among those owning the means of production in the form of financial capital to prefer rents and speculation (with their cash) over investment in “physical” capital; through influence the rentiers lower capital requirements and create an inherently unstable monetary structure, within which they fight like pirhanas over speculative opportunities, which leads to a cycle of intermediary collapses, extreme monetary base creation, and bailouts using sovereign powers of taxation to pass the loss along to the people; once trust on the monetary unit vanishes, perhaps with an expropriation of deposit funds, the stage is set for (1) deflationary collapse, as bank runs overwhelm the deposit insurance system, and (2) hyperinflation, as the monetary authorities order banks to issue prepaid debit cards to anyone wanting to withdraw his or her money from the bank to “restore confidence.” They then go and spend it as fast as they can.

The structural reforms needed: no more (or much higher reserve level) fractional reserve banking; steeply progressive income and, for a time, wealth taxation to restore a healthy circulation of income and product. See Emanuel Saez’s recent interview on this at http://www.bostonreview.net/BR38.1/emmanuel_saez_david_grusky_income_inequality_taxes_rent_seeking.php

Marx has the last laugh.

Personal note: the bank has cut my position, and I am seeking new opportunities. While I was happy to support small business lending, which is what I did, it was hard for me to reconcile working in such a manifestly corrupt industry as banking with my personal values. The Fed and the big banks are sucking the life blood out of the economy. As has recently become public knowledge, the big banks’ “profits” are manufactured out of their influence (being “too big to fail”). Still, small businesses need loans (sometimes), and I felt good about supporting that, although I would encourage anyone thinking of starting a small business to avoid debt if at all possible.

We are living through a period of history when the Devil has much of the world by the throat. One can only hope and pray that it ends better this time than it did in 1940. It will take a miracle of collective willpower.

My family was friends with Peter Drucker’s family when I was growing up. I recently got back in touch with Drucker’s daughter, about my age. Peter and Doris Drucker escaped from Austria in 1937 for America. They were concerned about the Nazis. Both Druckers were of Jewish extraction.

Peter died years ago, but Doris, a brilliant woman, lives on in Southern California, now 102. I asked my friend if her mother saw any similarities between what is happening in America now and what she saw in the 1930s in Europe.

“My mother is paranoid,” my friend said. “She’s says we need to keep cash on hand to bribe the guards at the Canadian border.”

Go read Jim Quinn’s last few posts at www.TheBurningPlatform.com— “No hesitation targets” and “Wall Street titans screw you every day”.

Source: FRED. Data to 2012Q4. The blue line is the value of the most recent observation. Almost every other time this value has been seen the economy has been either going into recession imminently, or within a year or so. Only in the 21st century has the economy managed to avoid recession by bouncing off the blue line.

The green line is linear trend over the period from 1950. The red line is the trend over the past 30 years, which suggests that the US economy is headed for a state of secular stagnation and possible collapse.

N.B. This is research, not investment advice. You invest at your own risk, unlike the Wall Street banks, who also invest at your risk.

The uptick of the unemployment rate from 7.8 to 7.9 has caused our ‘animal spirits’ indicator to put in a top. Continued increases or merely stability of the unemployment rate will cause further losses of confidence.

The underlying judgmental unemployment rate forecast is this:

My forecast is still that the US economy enters recession in the second half of 2013. The two big proximate drivers: the continuing assault on consumption from higher taxes and medical costs; a precautionary demand for liquidity (increased saving rate); the sequester—to any degree—of federal government spending; and to the extent that it impacts the small segment of the population current salivating over stock market gains induced by QEternity, a diminished wealth effect (yes, the implicit stock market forecast is that we’re at a major top—I called it a year ago but the presidential election year got in the way—this cycle is very reminiscent of the early 1970s, and we’re at about the turn from 1972 to 1973). Throw in Europe in various states of severe recession and depression, and the likelihood of some slowdown in China, and we have the potential for a coordinated global contraction, almost as if the signs all say we are at the end of the [high?] growth age….

Here is the whole history:

Note how depressed the Michigan Consumer Sentiment index is, just as it was in the early ‘Seventies. The drop-off from here could be precipitous from here. Even somewhat proven indicators such as the “Rule of 20” show the market looking toppy (yellow line is where the blue S&P line is supposed to be):

Source: News-to-Use

I’m going to keep this short and sweet.

It ain’t tax cuts. Federal revenue as a percent of GDP is already way below long term averages, and it was already probably too low--we have a decaying infrastructure to show for it.

It ain’t “stimulus spending.” The Princeton Clowns, Krugman and Bernanke (and remember, Princeton historically has sent more of their graduates to Wall Street than any other school in the country) with some fact-checking by the Berkeley Inequality Guru, Emmanuel Saez, have shown the rest of us that stimulus spending, like all other income types, goes mostly to the top 1 percent. Saez showed that in 2010, a year when the stimulus package was active, 93 percent of the increase in income went to the top 1 percent.

I can picture Krugman and Bernanke as two nerds playing with the rubber nipples of a blow-up woman doll, one nipple labeled “fiscal policy” and the other labeled “monetary policy.” Heads up their asses, fully captive to the status quo.

So what works? Income redistribution. You take money, whether borrowed or taxed, and give it to the people on the bottom. They will spend every penny of it, and it have a multiplied effect on many other incomes. While they may buy goods made in China by American corporations sold at Walmart, they are likely to spend a lot of it on goods made right here at home.

The Benign Brodwicz program has always been poverty level workfare for those that need work, and honest banking. If the honest bankers in the world would think for a second, they might realize that it was playing extend and pretend to recapitalize after the Latin American debt collapse in the 1980s that started the country on its own debt run-up.

File under kleptocracy, banana republic, fascism, theft

Assume that capital is mobile internationally, and it will seek the highest net rate of return. It is evident that consumption has been overweighted in the composition of American aggregate demand, because it was debt-funded. Increasing income and wealth inequality lower the average propensity to consume. Disposable income is being reduced by tax increases. Investment demand is largely derived from the demand for final goods, for which capital goods are used in production. With stable or decreasing final consumption demand, investment demand is largely put on hold. In this essentially deflationary situation, slack appears in labor and industrial markets. Capital sits on the sidelines, waiting to see what happens next, where the greener pastures may lie. Central bankers lower interest rates to the zero bound and sit around wishing and hoping for an inflation to get the debt under control. Sovereign governments, beholden to the banks, refuse to use the issuance of sovereign currency to put slack assets back to work. This is where we find ourselves.

The conventional wisdom, as given on personal finance websites and in corporate boardrooms, is to wait for the turn of the developing economies, and to put the money where the growth is. America is unattractive.

There is much damage being done to the world economy while playing this waiting game. One by one, developed economies are being sent into severe depression, for example, Portugal, Greece, Spain. These poor countries had unfortunately given away the right to manage their own currencies and were crushed by German creditors. The Japanese, under no such constraints, are gearing up to devalue their currency in an aggressive, mercantilist strategy. Can Brazil, Russia, and India be far behind? China is attempting to balance their domestic demand, and we wish them well. The United States has pushed its interest rates to zero but is frustrated by the status of its currency as the "risk-free" asset. The US has shown that it can blow asset bubbles but because it is intent on the continuing crucifixion of its labor class, it cannot get a sustained domestic inflation going. Pity the poor greenback.

The hidden shoals of the international financial system, the derivatives exposures so conveniently not on the banks' balance sheets, guarantee that the chances of international collapse of the deflationary type are still significant. At that point, should it arrive, some new form of money will almost certainly need to be created. The Fed buying up all Treasury issuance will not be enough.